Europe’s Financial Data Access (FiDA) framework promises to reshape the region’s financial ecosystem. By extending the principles of Open Banking beyond payments into broader Open Finance, FiDA will enable consumers and businesses to securely share their financial data with trusted third parties to access better products, advice and digital experiences.

But for all its promise, FiDA also introduces a new layer of complexity, especially for data holders (financial institutions) such as banks, insurers and investment firms. One of the biggest challenges they face is a deceptively simple question: “How do financial institutions know who is allowed to access what data and when?”.

Under FiDA, every financial institution (i.e. a data holder) across the European Economic Area (EEA) must verify the identity and status of any third party requesting access to customer data (a Financial Information Service Provider, or FISP). Specifically, the data holder must confirm that the FISP:

- Is authorised under FiDA

- Is authorised in the jurisdiction in which it is requesting to operate

- Participates in a relevant FiDA scheme(s)

- Is requesting access within the scope of its regulatory and scheme permissions

- Has obtained valid customer consent for the requested access

This paper explores why that’s so difficult, what risks it creates and how financial institutions can prepare.

Why Data Access Verification Matters

FiDA is designed to empower consumers to control their financial data. It builds on the success of European Open Banking (i.e. PSD2) but goes much further, covering savings, investments, insurance, pensions and credit.

To make this possible, data users such as fintechs, advisors and aggregators will be able to access customer data from banks, insurers, investment firms and other providers, but only if:

- The data user (i.e. FISP) has the right regulatory and scheme authorisation for that type of data

- The customer has given explicit consent

This means that financial institutions must check both the FISP’s permissions and the customer’s consent before granting access. The difficulty lies in doing this accurately, instantly and across borders in the EU.

Complexity Beneath the Surface

In Europe, financial institutions are authorised and supervised by the national regulator (i.e. National Competent Authority – NCA) in their domestic (“Home”) Member State.

Whilst at a European level the European Banking Authority (EBA), European Securities and Markets Authority (ESMA) and the European Insurance and Occupational Pensions Authority (EIOPA) maintain some central high-level registers, the reality is that each country still uses its own systems with different formats, languages and update frequencies.

As a result, the regulatory landscape is fragmented with no single EU-wide database that allows financial institutions to instantly verify whether a data user (i.e. FISP) is:

- Authorised under FiDA

- Authorised in the jurisdiction in which it is requesting to operate

- Participates in a relevant FiDA scheme(s)

- Is requesting access within the scope of its regulatory and scheme permissions and

- has obtained valid customer consent for the requested access

Different Data Domains, Different Rules

FiDA doesn’t open up “all financial data” to everyone. Instead, it defines categories, such as:

- Payment accounts

- Investments

- Insurance products

- Loans and credit data

Each type of data has different rules (as defined by a relevant FiDA scheme) about who can access it. So, a FISP authorised to handle investment data will not be allowed to access insurance or mortgage data, even with the customer’s consent. In order to access these other data sets, FISPs will need to be members of other relevant FiDA insurance/mortgage schemes.

For financial institutions, it means they’ll need to build fine-grained mappings between their internal data sets and FiDA’s regulatory categories, something few organisations will have today.

The Cross-Border Puzzle

FiDA, like PSD3 & PSR, supports the concept of passporting, which means a FISP authorised in one EU country can operate in others, once regulatory permission has been granted.

Therefore, as an example, if a Lithuanian FISP requests data from a Spanish bank, the Spanish bank must:

- Confirm the Lithuanian FISP’s licence is valid

- Check that the FISP’s passport for Spain is valid

- Confirm that the FISP is a member of the relevant FiDA scheme

- Make sure the consumer consent aligns with both Lithuanian and Spanish rules

- Ensure that the data requested aligns with the FiDA scheme data set(s)

Each step adds layers of operational complexity, especially without a unified European verification tool. Even if a customer says “yes” and consents to data sharing, that doesn’t automatically mean the FISP has the legal authority to access the data.

In FiDA:

- “Consent” comes from the customer

- “Permission” comes from the regulator

- “Membership” comes from the FiDA scheme

Financial institutions must check each of these elements to ensure they match. For example, if a FISP’s authorisation doesn’t cover the requested data type, or they are not a member of a relevant FiDA scheme, the financial institution must deny access, even if the customer has agreed.

It is important to note that under FiDA, the number of third parties will increase dramatically compared to those authorised under PSD2. On top of this expansion in numbers, additional layers of complexity will further complicate the ecosystem.

FISPs may be registered to operate in a single country, across multiple jurisdictions, or even EU-wide. They may also belong to one or several FiDA schemes. National Competent Authorities can suspend or revoke FISP licences, as already observed under PSD2; and schemes themselves may terminate a FISP’s membership. As a result, the environment will be highly dynamic; FISPs will enter and exit the market, cease trading, be acquired, or change the scope of their regulatory authorisations. In short, the landscape will not be static but characterised by continual movement and change.

To satisfactorily manage risk and ensure that there is no unauthorised access to customer data, financial institutions must:

- Continuously monitor the status of each FISP they interact with

- Revoke data access immediately if a FISP licence changes

- Revoke data access immediately if a FISP does not have the relevant passporting permissions

- Understand which scheme(s) a FISP is a member of and its associated permissions

- Keep detailed logs to prove compliance to regulators

Risk management and risk mitigation are not a one-time check; they are an ongoing process. FISPs’ authorisation(s), passporting rights and scheme membership(s) will continually change. To protect themselves and their customers, it is incumbent on financial institutions to understand what a FISP’s status is at the time a customer data access request is made.

The Challenge for Financial Institutions

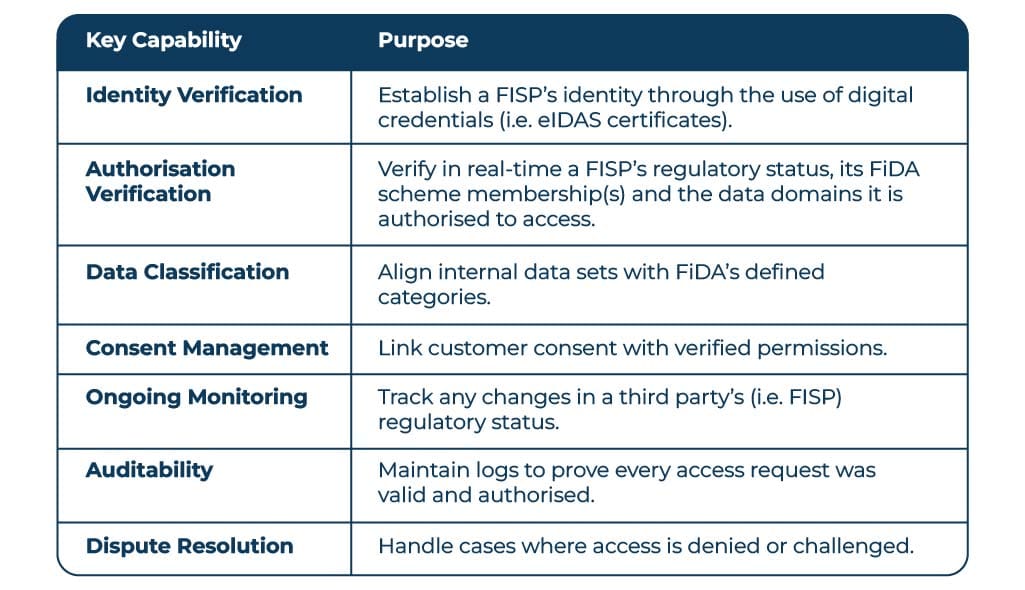

Financial institutions will need to build new capabilities to manage this complexity.

A Vision of the Future

To make FiDA work smoothly, the ecosystem will need common identity and verification infrastructure and shared standards including:

1. A Central European Registry

The EBA is tasked with maintaining central registers of all PSD3, PSR & FiDA authorised entities; however, it should be noted that the EBA does not take liability for the data in the registers, its quality, consistency or timeliness of updated information. It will not provide the fine-grained mapping between Data Holders’ and FISPs’ membership of relevant FiDA schemes. This means there is no single source of “truth” that European financial institutions can reference to understand the validity of a FISP’s licence, its passporting permissions for specific jurisdictions and the FiDA scheme(s) of which it is a member.

2. Linking regulatory authorisation to strong digital identity certificates (eIDAS)

Linking regulatory authorisation to strong digital identity certificates would enable a data holder to automatically verify a TPP’s identity when it connects to an API. However, unlike under PSD2, certificates should be used solely for what they are designed to provide: cryptographic proof of identity, not proof of regulatory status or permissions.

Authorisation, regulatory permissions and Scheme(s) membership are dynamic: they can be granted, amended, restricted, suspended, or withdrawn over time. Embedding those permissions into a certificate at the point of issuance creates a static snapshot that can quickly become inaccurate. Relying on such certificates for authorisation and regulatory permissions in isolation is insufficient and risky. It could result in a financial institution continuing to grant access to a third party whose regulatory status has changed without that change being reflected in the certificate.

For this reason, identity (who the TPP is) should be established through its eIDAS certificates, whilst authorisation (what the TPP is permitted to do) should be verified against an authoritative, up-to-date regulatory register at the time of access.

3. Industry-Led Utilities

National banking associations or European consortia could develop shared “authorisation gateways” to simplify compliance.

An example could be whereby a shared authorisation gateway acts as a trusted intermediary that:

- Centralises verification of third parties’ credentials and their regulatory status

- Issues or validates tokens/certificates for secure API access

- Provides a unified trust and identity layer for all participating entities

Such an approach can deliver simplified compliance, lower integration costs, improved security and simplified interoperability, supporting and underpinning innovation.

4. Risk-Based Access Controls

Financial institutions could tailor the level of verification to the risk profile of the requesting party (i.e. FISP), balancing compliance and innovation. However, arguably this becomes a little difficult and complex in an European open finance (FiDA) context, as FISPs are regulated entities and therefore cannot be denied access if they can: a) prove their identity (e.g. eIDAS certificate), b) have the appropriate regulatory authorisations and the right to operate within the given jurisdiction, and c) are a member of a relevant FiDA scheme(s).

However, the financial institution does have the ability to decline a data/payment request if: a) the consumer/business has not provided explicit consent, b) the FISP does not hold the relevant authorisations, c) it believes that there is suspicion of fraud or malicious activity or d) that fulfilling the request would violate other legal or regulatory requirements.

Europe is Unique however there are Lessons to be Learnt

Europe is unique as a political and economic union, combining supranational governance, deep economic integration and legal harmonisation. This structure delivers substantial benefits to Member States, their economies, businesses and citizens, but it also creates a level of institutional and regulatory complexity that shapes how open data-sharing frameworks are designed and implemented.

That complexity is particularly visible in open finance. Europe’s model of EU-level rulemaking, combined with national-level supervision, enables strong cross-border consistency; yet it also requires careful coordination to ensure that legal, supervisory and technical frameworks operate seamlessly across Member States. These challenges are most evident in the cross-border data-sharing regimes that will be established under PSD3, the PSR and FiDA, where common technical standards must function within diverse market and supervisory environments.

However, jurisdictions that were able to build on the lessons learned from PSD2 have had the opportunity to embed strong technical and governance frameworks into their open banking and open finance ecosystems from the outset. This has helped provide consumers and businesses with greater confidence that their data is shared securely, only with authorised third party providers and strictly in accordance with the consent they have given.

A feature common to many of these newer implementations is the use of shared technology infrastructure that supports the entire open banking or open finance ecosystem. Such infrastructure can provide a consistent foundation for identity, security and regulatory verification, strengthening trust, reducing friction and supporting scalable cross-border data sharing.

A Single Unified Central Directory (Source of Truth) Underpins the Success of FIDA

Trust, confidence, security, control and regulatory certainty are all prerequisites to underpin a thriving, successful open data sharing ecosystem. Trust and confidence are the lifeblood that give users (i.e. consumers and businesses) the confidence to engage in open finance services to deliver better outcomes and personalised services that are tailored to meet their specific needs and requirements.

For FiDA, a single, unified central directory, (delivered by an organisation with the capability to collect data from varied and disparate sources in real time that standardises and normalises the data, to correct missing or inconsistent information and to keep it continuously aligned with the legal systems of record), will deliver the trust, confidence, security, control and regulatory certainty to deliver effective FISP verification.

This would deliver:

- Real-time FISP identity validation via digital certificates connecting to Qualified Trust Service Providers (QTSPs) and revocation lists

- Automated monitoring of NCA registers to provide real-time FISP authorisation accreditation and passporting rights

- Automated monitoring of FISP scheme(s) membership to know which data sets can be accessed

- Timestamped data to demonstrate when data changes occur

- Cross-checks with national competent authorities for ambiguous or high-risk cases

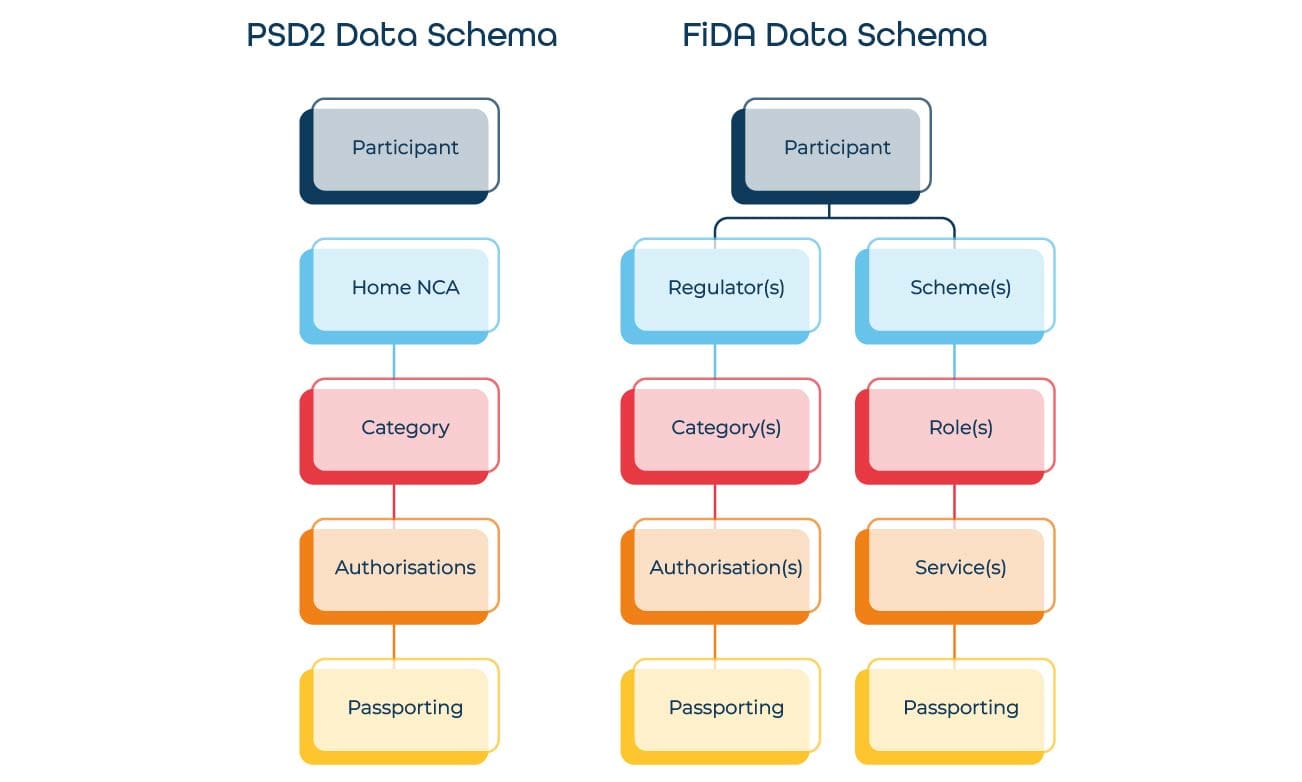

Unlike the transition to PSD3, the scope of data under FiDA is broad and draws on multiple data sources. Under FiDA, European Open Banking (PSD2) will become one of several schemes of which a Participant may be a member, alongside, for example, investment schemes, insurance schemes, mortgage schemes and pension schemes.

Participants may be overseen by multiple regulators/NCAs. In Italy, for example, these would include:

- Italy Banking & Payments: Banca D’Italia

- Italy Insurance & Intermediaries: IVASS

- Italy Investment Firms & Securities: CONSOB

A Participant may also be assigned different identifiers by the different regulators, each following its own format, for example:

- IT-BI-00000

- IT-IVASS-11111

- IT-CONSOB-22222

A single unified central directory underpins the success of FIDA, removing complexity and delivering trust, confidence, security, control and regulatory certainty to financial institutions and – by definition – to their customers.

Turning Compliance into Opportunity

While these requirements may look like a burden, they also create opportunity. By investing in secure, transparent authorisation frameworks, financial institutions can:

- Build greater trust with consumers and regulators

- Reduce friction when onboarding new fintech partners

- Offer “trust services” or verified access gateways as new commercial products

- Position themselves as data custodians of choice in the open finance era

Over time, solving the authorisation challenge can become a competitive advantage, not just a regulatory obligation.

FiDA represents the next major step toward a truly open financial ecosystem. For it to succeed, however, Europe needs a reliable and harmonised way for financial institutions (as data holders) to verify the permissions of those requesting access. Without this infrastructure, financial institutions face a difficult balancing act: protecting customers and complying with regulation, while avoiding unnecessary barriers to innovation.

In this context, FISP verification becomes the new frontier. Knowing who can access which data and under what conditions is one of the most complex challenges under FiDA.

The financial ecosystem is changing. New technologies, expanding data sets and open data frameworks are creating fresh opportunities, but also new and evolving attack vectors. For financial institutions, security and resilience must therefore be continuous with adaptive capabilities, not static controls. Defences, systems and governance must evolve in step with innovation to protect both customer data and institutional integrity.

Trust remains the foundation of open banking and open finance. Customers will only share their data if they believe it is secure and used responsibly. Strengthening that trust through proactive security, robust oversight and collaboration is therefore not just a compliance requirement, it is a strategic imperative for growth and competitiveness in the open data economy.

As FiDA expands open banking into open finance, authorisation, identity and cross-border verification must move beyond fragmented national registers and static, point-in-time checks. A resilient ecosystem depends on real time validation of regulatory status, scheme membership and data permissions, underpinned by strong digital identity and continuous monitoring.

Konsentus provides real time third party verification and maintains a continuously updated Directory of authorised participants, helping ensure that innovation in open banking and open finance remains firmly anchored in trust, compliance and control.

Get in touch to explore how we can support your FiDA readiness and strengthen your long-term open finance resilience.

Brendan Jones

COO, Konsentus